L’ACI met à jour ses prévisions pour le marché résidentiel de la revente Les ventes se sont stabilisées depuis le début de 2021, mais l’offre restreinte devrait continuer de faire monter les prix

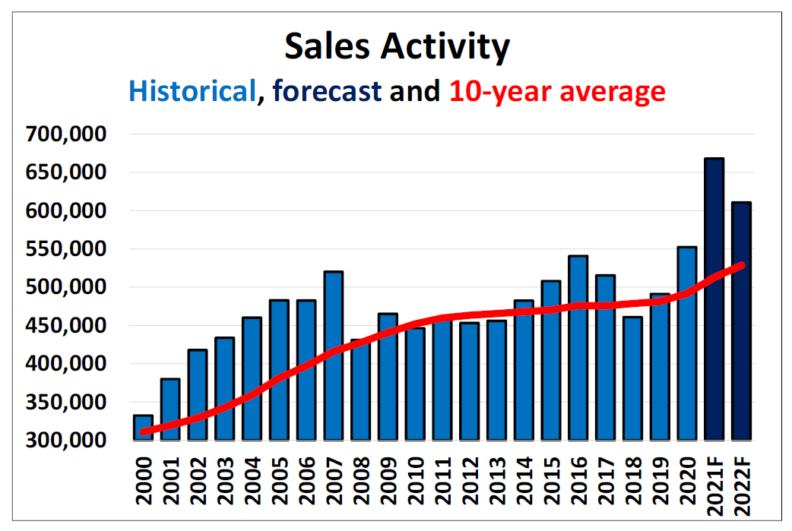

Over the past several years, record levels of international immigration (not including 2020), low interest rates, and an increasingly middle-aged Millennial cohort have come together to fuel very strong household formation and housing demand in Canada. Recall that prior to COVID-19, the number of available listings nationally was already at a 14-year low and the national number of months of inventory on the eve of the lockdowns had fallen to below 4 months (seller’s market territory).

COVID-19 only served to supercharge trends that were already present, with even stronger first-time home buying activity teaming up with a surge in existing owners choosing to pull up stakes – everyone trying to find the right place to ride out the pandemic. At the same time, many other existing owners who may have made their homes available to buy in a normal year simply hunkered down. This served to drive prices sharply higher while supply fell further to reach all-time lows. The good news is that the urgency and frenzy of earlier in 2021 have started to fade and the market has settled down a bit, at least in a relative sense.

At this point most housing market indicators appear to be leveling off at a cruising altitude somewhere in between pre- and peak-pandemic levels. The exception is the end-of-month inventory of properties for sale, which continues to hit fresh lows. As such, the market remains historically imbalanced, which could have unprecedented implications for, and presents unprecedented risks in forecasting, both the number of sales and the price of those sales.

Supply concerns aside, the mass vaccination of society and (eventual) reopening of our lives and economies along with the associated migration and international immigration also present a considerable amount of uncertainty to the outlook over the balance of 2021 and into 2022, but only from a timing standpoint. It is hard to see how these will not ultimately act as tailwinds for housing demand. 2021 will almost certainly be a record year for home sales in Canada. While 2022 is expected to see significantly fewer MLS® transactions than in 2021, it is nonetheless still expected to mark the second-best year on record for Canadian home sales.

Of course, another risk to the forecast is the federal election in which ideas on how to fix the housing market have taken a prominent place. While it has been encouraging to see all the major parties looking at longer-term solutions to the supply shortage issue, it also highlights how there are no quick fixes. As anyone who has tried to get even a small project done in the last year knows, availability of materials and skilled labour are not dials that can simply be turned up to 11 whenever we decide we need them. And that’s not to mention all the other barriers to building, of which there are many. So it may be easier said than done, but the conversation is a welcome change after a decade of demand-side tweaks. We’ll see what initiatives are kicked off after September 20.

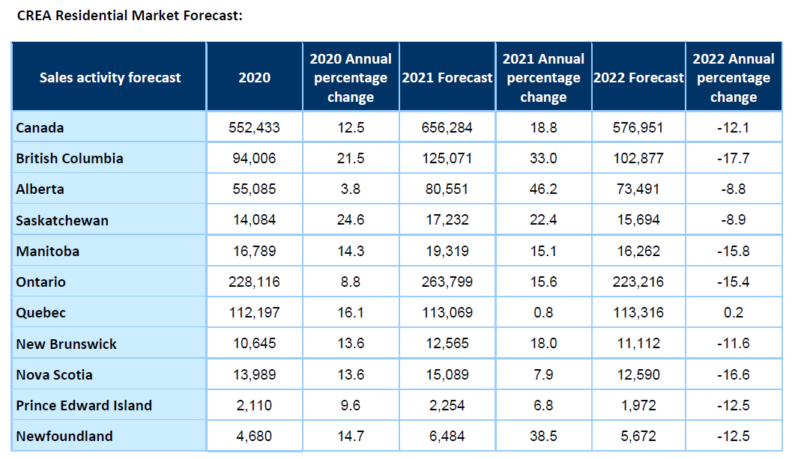

Some 656,300 properties are forecast to trade hands via Canadian MLS® systems in 2021. This would be a record-setting number, and an increase of 18.8% over 2020. That said, this forecast does represent a downward revision from previous estimates, as sales fell more rapidly than predicted this spring.

The strength of demand in 2021 has been geographically broad-based and CREA anticipates strong sales growth in every province with the exception of Quebec, where the second half of 2020 was comparatively stronger than the first five months of 2021. That said, timing aside, we are well past the peak of activity everywhere at this point.

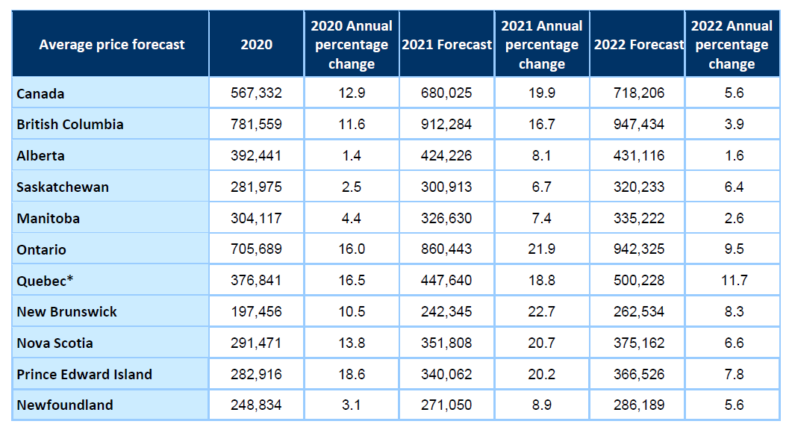

The national average home price is forecast to rise by 19.9% on an annual basis to $680,000 in 2021, little changed from CREA’s previous forecast. This historically large increase reflects the current unprecedented imbalance of supply and demand, still close to 2 months of inventory nationally.

On a monthly and quarterly basis, sales are forecast to continue trending slowly back towards more typical levels through the latter months of 2021 and into 2022; although, it is possible that most of that has already happened. Limited supply and higher prices are expected to tap the brakes on activity in 2022 compared to 2021, although increased churn in resale markets resulting from the COVID-related shake-up to so many people’s lives may continue to boost activity above what was normal before COVID-19. Indeed, it is possible that many of the moves associated with changes related to remote work won’t play out until further down the road when we have more certainty about what the future will look like post-COVID.

National home sales are forecast to fall by 12.1% to around 577,000 units in 2022. This easing trend is expected to play out across Canada with buyers facing both higher prices and a lack of available supply, while at the same time the urgency to purchase a home base to ride out the pandemic continuing to fade. Still, with supply at record lows, the national average home price is forecast to rise by 5.6% on an annual basis to around $718,000 in 2022.

- 30 -

About the Canadian Real Estate Association

The Canadian Real Estate Association (CREA) is one of Canada’s largest single-industry associations. CREA works on behalf of more than 135,000 REALTORS® who contribute to the economic and social well-being of communities across Canada. Together they advocate for property owners, buyers and sellers.

For more information, please contact:

Pierre Leduc, Media Relations

The Canadian Real Estate Association

Tel.: 613-237-7111 or 613-884-1460

E-mail: pleduc@crea.ca