Mixed Signals in Canada’s Commercial Real Estate Market: Commercial Snapshot Q3 2024

Each quarter, the Canadian Real Estate Association (CREA) publishes a summary of key economic indicators for commercial real estate in Canada. Housing starts, non-residential building permits, gross domestic product (GDP) and the labour market are routinely monitored by CREA’s economic team as predictors for the commercial real estate market. For residential market information, visit CREA Stats.

Looking at commercial real estate data for the third quarter of 2024, the Canadian Real Estate Association (CREA) sees evidence of a mixed commercial real estate market across the country. A rise in the value of non-residential building permits issued is being offset by challenges in developing new housing, a weakening employment market, a lower Canadian dollar, and the threat of tariffs on Canadian exports entering the United States.

The value of non-residential building permits issued rose by almost 9% compared to the second quarter of 2023, owing to stronger intentions to build industrial facilities across the country.

The Department of Finance has announced changes to mortgage rules which should spur construction in new housing starts, however, they’re still coming in well-below levels observed in 2021 and 2022. Challenges facing the housing sector are numerous, including high material and labour costs, high land values, and permitting/regulatory hurdles.

The labour market continues to show signs of weakening. There are more people in Canada entering the labour force than there are getting jobs, and many younger Canadians and newcomers are finding it difficult to secure employment. Some companies are looking to decrease their headcount amidst slower sales and a weakening economy, and the federal government is making changes to its temporary foreign worker program.

For the commercial real estate market, 2024 continues to be challenging as borrowing and construction costs remain high, and transactions remain at below average levels. However, the lowering of interest rates that began in the summer is starting to make it more financially feasible to bring new product onto the market. If interest rates continue to decrease as is forecasted market activity could pick up further in 2025.

Here’s a deeper look into some of the data CREA is monitoring as it pertains to commercial real estate.

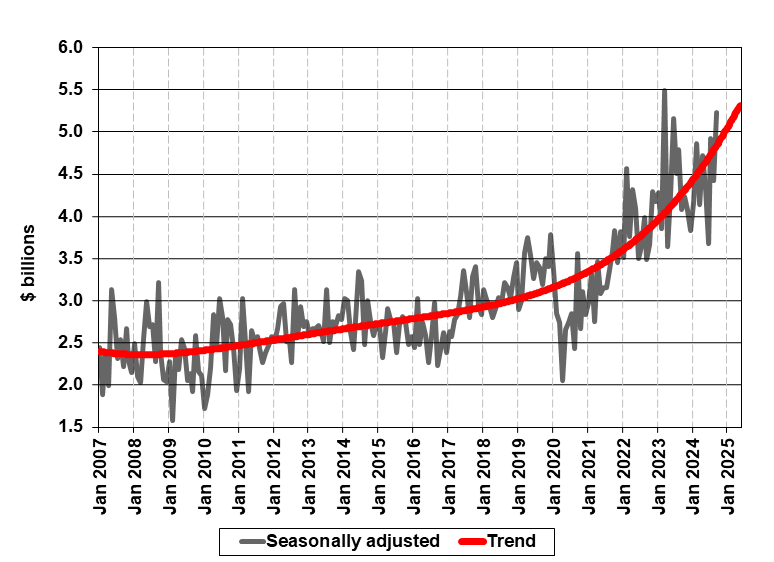

Non-Residential Building Permits

Approximately $14.58 billion in non-residential building permits were issued from July to September 2024. This was up close to 9% from the same three-month period a year ago, and a 14.6% jump from the three months prior. Notable activity observed across the institutional and industrial subsectors.

Major projects in Ontario helped drive national gains in the institutional and industrial component. Ontario’s institutional component received significant boosts from plans to build long-term care facilities across the province and a hospital permit in Prince Edward County. Investments to help build up battery supply chains in Ontario and Quebec, as well as general growth in other provinces, helped push the national industrial dollar value in permits to a record high.

While the industrial sector has seen an upturn in investment since interest rates started to fall, the commercial component continues to face significant challenges and weaker investment.

A weakening Canadian dollar and proposed tariffs on Canadian exports to the U.S. may bring challenges to the non-residential sector moving into 2025, with larger institutional and governmental projects expected to make up for some of the shortfall expected in the private sector.

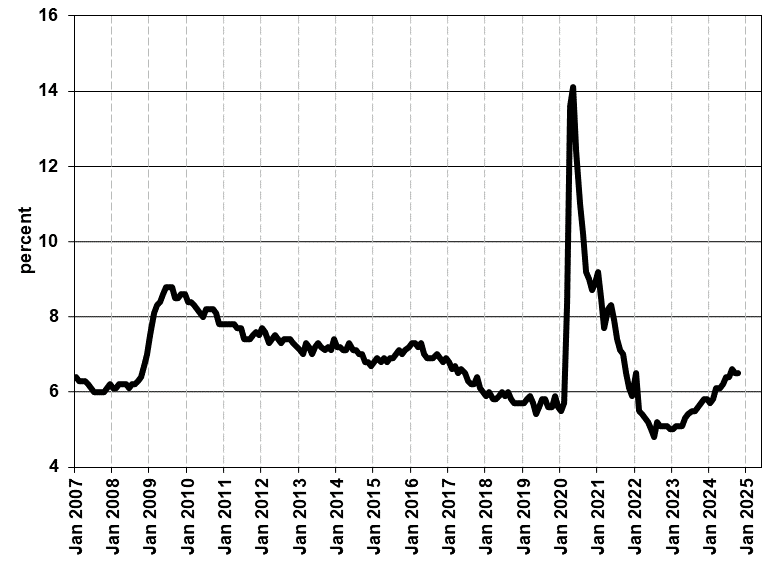

Labour Market Dynamics

The national unemployment rate in Canada held steady at 6.5% in October 2024, underscoring cooling labour market conditions amidst a slowing economy.

Near record-levels of population growth in Canada over the last few years continue to influence the labour market, with employment growing more slowly than the labour force in recent months and job seekers taking longer time to find work. Younger Canadians and newcomers to Canada are having the most difficulty in finding work.

Many employees feel the overall cost of living has outpaced wage growth in recent years, which is one of the reasons we have seen trade unions across critical industries such as railway, port workers, and Canada Post authorize strike actions over the last few months.

The federal government has announced it intends to reduce immigration levels over the next two years, specifically international students, and foreign workers, amidst reports of abuse in the system. It has also signaled a shift to Canadian employers using the temporary foreign worker program, requiring them to try to recruit Canadian workers before filling job openings with temporary foreign workers.

According to the Bank of Canada’s Third-quarter 2024 Business Outlook Survey, with a slowing economy, the share of companies reporting labour shortages are considerably less intense than a year prior, and expected future wage increases over the next year have also declined sharply.

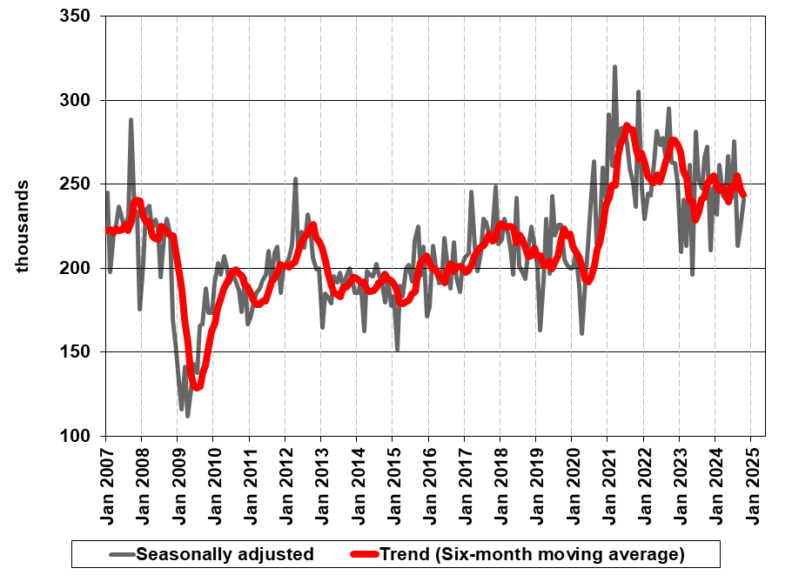

Housing Starts

Canadian housing starts barely budged from January to October 2024, compared to the same period in 2023, but are much weaker than levels seen in 2021 and 2022.

Growth in year-to-date housing starts were driven by higher multi-unit and single-detached units in Alberta, Quebec, and Atlantic Canada. This growth offset lower starts in Ontario and British Columbia.

The Department of Finance has announced upcoming changes to the Canadian mortgage charter, increasing the price cap for insured mortgages from $1 million to $1.5 million, and expanding 30-year amortizations to all first-time home buyers and to all buyers of new builds. This may help spur the creation of new housing units in 2025 and beyond.

Constraints on new housing construction, such as the availability of land, zoning, and regulatory restrictions, permitting delays, rising costs in borrowing and construction, and a lack of skilled labour, continue to make it challenging for homebuilders to bring on new supply at a quick and affordable pace.

A report by the Canadian Mortgage and Housing Corporation highlights the impact that government fees and permits add to new supply, often resulting in fees that potentially increase the cost of new home construction by as much as 30% in some markets.

A report by the Conference Board of Canada, produced in conjunction with CREA, the Ontario Real Estate Association (OREA), and British Columbia Real Estate Association (BCREA), highlighted that Canada needs to fill 12,000 skilled labour vacancies per year in the residential construction industry over the next decade to meet our country’s housing needs, and non-traditional sources of construction labour will play a crucial role in filling those vacancies.

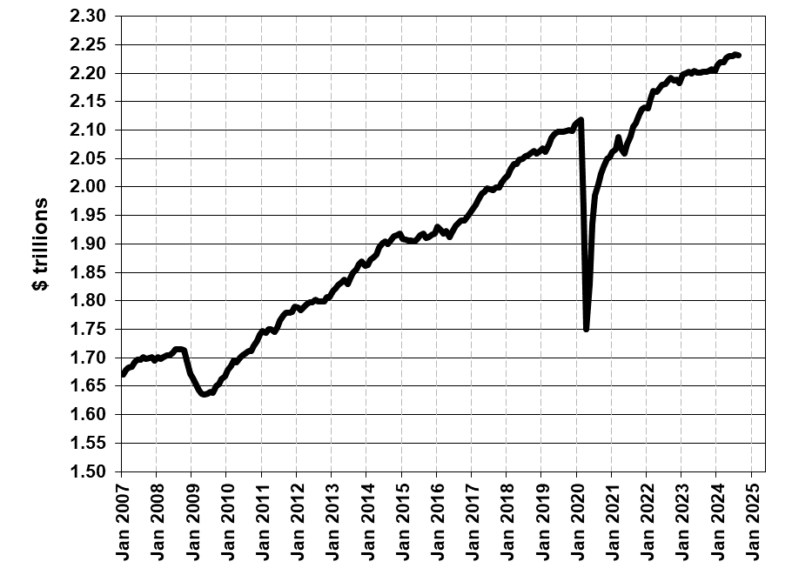

Gross Domestic Product (GDP) Growth

In its October 2024 Monetary Policy Report, the Bank noted that economic growth in the second quarter was slightly stronger than expected, while the third quarter looks weaker. Economic growth is expected to pick up and average 2.5% over the next two years.

On a per capita basis, gross domestic product (GDP) contracted for the fifth consecutive quarter, as inflation-adjusted growth in the economy has not kept up with population growth. Real GDP per capita is expected to continue to trend lower as we move into the second half of the decade. Senior leadership at the Bank of Canada have described this as a national emergency.

Consumer Price Index (CPI) inflation continues to trend at its 2% target but prices for food and the shelter component continue to prop up overall inflation. As households adapt to higher borrowing costs and the higher cost of living, they’re allocating a larger share of their income to servicing debt and spending less on discretionary items such as consumer goods, eating out, and travelling.